Values plummet in the Fresh Produce sector as the bad news keeps rolling in

If ever there was a market that has had to navigate unrelenting turbulence over the past few years it’s the UK Fresh Produce industry.

First, we had the pandemic. The shutting off of the hospitality trade saw demand for fresh produce completely cut off. Granted, consumer demand may have replaced some of that lost restaurant and hotel trade as we all tried to get healthy and live like Joe Wickes but the loss of demand hurt.

Then we moved out of the pandemic directly into Brexit chaos. Loss of unfettered access to the single market, queues of lorries at Dover, reams of paperwork to move produce, a dearth of seasonal staff to pick things out of the ground and pack it, the list of disruptions from our withdrawal from the EU is long and growing. The Northern Ireland problem could well be the start of even worse issues.

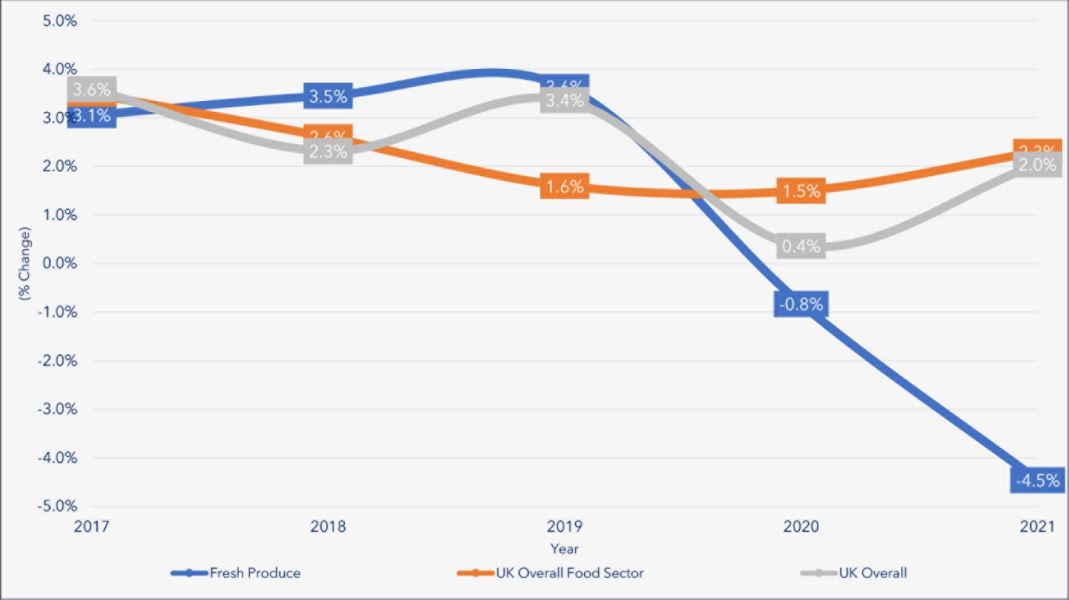

The list of other macroeconomic factors unsettling the market such as soaring energy costs, National Insurance increases and Ukraine and all the other things that continue to buffet the market. But let’s move on to how all of these challenges are impacting the market. Overall valuations are down 4.5% in the latest year. That compares to a 2.3% increase across the wider food sector.

Values across the market are falling with almost half of all the firms Plimsoll has assessed losing 10% or more of their value. Only 120 firms have seen their value rise over the last few years.

The change in values over the last two years has been the starkest. While the rest of the food sector has seen a fairly steady rise of 2-3% over the last years, with a slight uptick in the latest year, fresh produce has seen major pressure on business values and they are down 4.5% in the latest year. That follows a 1% fall in the preceding year. For context, in 2018 Fresh Produce had one of the highest value growth numbers of any food industry.

Within the industry, there is a growing divide in valuation performance based on size. The 10 largest companies within the market have lost around 2% of their value. In contrast Companies under £4m turnover have, on average, shed 16% of their value in the same period. There is a group of middle-sized companies that have seen values rise but they are something of an outlier in the market.

The final area worth mentioning is the niches within the wider sector. It was interesting to see that the most impacted part of the produce sector has been importers. Clearly, Brexit and soaring costs of shipping or bringing products into the country have decimated that part of the market having knocked 6% off average values. Prepared and frozen vegetables have also seen a marked decline in average values.

Of course, it's not all doom and gloom. Purveyors of organic produce have seen enormous growth in average values – up 18%. Similarly, domestic soft fruit growers have seen values up 5% despite all the issues regarding picking and packing produce and the sales routes into becoming the single market increasingly fraught.

It is clear that the Fresh Produce industry is under increasing pressure and without an end in sight to the disruption affecting the market, the malaise is likely to continue. To find out more about the Fresh Produce industry, and where your business compares against competitors, head to https://landing.plimsoll.co.uk/fresh-produce-insight to claim a free insight report and discover the potential of the analysis creating this data.