Business values continue to be depressed in the Waste Management sector

Waste management is going through a period of flux as the sector fragments into shifting lifestyle trends, increased end-user convenience and macroeconomic shifts.

First, we had the pandemic and the shutting down of festivals, sports events and other large-capacity gatherings. Then the recalibration and rebalancing of everyday life to a hybrid model of office and home working has changed the landscape in the waste sector.

As we have moved past the pandemic and the economy has reopened, demand has increased in areas such as construction, medical and drilling waste management. However, the sector faces significant cost challenges. The new trade barriers and red tape to transporting the millions of tonnes of refuse-derived fuel (RDF) into and out of the EU after Brexit will increase costs. The sector is also vulnerable to the increased cost of fuel and energy with transportation a significant cost in all parts of the sector. How much of the increased cost can be passed on to overstretched end users?

There are several other macroeconomic factors unsettling the waste market including the dearth of staff and wage pressures. But let’s move on to how all of these challenges are impacting the waste market. Overall valuations are still rising but at a much lower rate than before the pandemic.

The top level average masks some serious fragmentation in business value by size of company and the niche markets served within the wider sector. In total almost a third of the UK’s leading waste companies saw their value fall by at least 10% in the latest year despite the recovery in economic activity. Only 241 firms have seen their value rise over the last few years.

Within the industry, there is a growing divide in valuation performance based on size. The 10 largest companies within the market have seen values plunge 18% - the biggest fall in the sector by some margin. Why have the household names in the waste sector performed much worse than their smaller counterparts? In contrast Companies within the £4-10m turnover range have, on average, values risen by almost 10% in the same period. However, the micro companies in the market, with revenue below £2m have seen values fall by 6%.

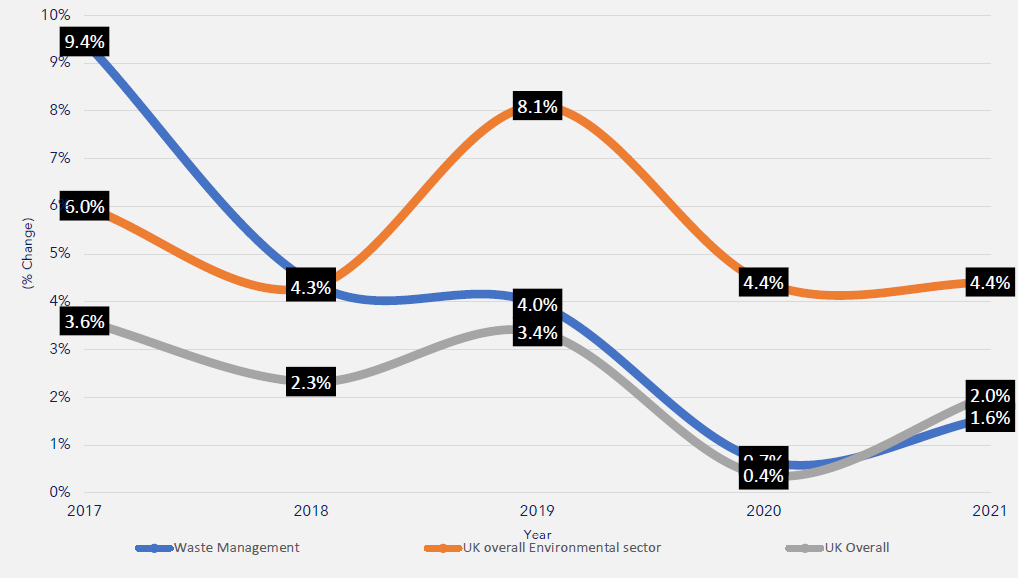

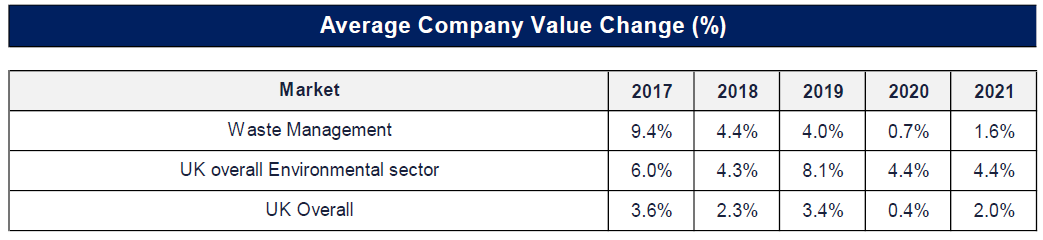

According to the latest Plimsoll Analysis, the average company values across Waste Management have risen in the latest year by around 2%. That’s more than double the 0.7% rise we saw in the previous, pandemic-ravaged year but lags behind the wider Environmental Services sector where average values are up 4%. In fact, across the environmental sector values have risen by more than 4% in each of the last two years.

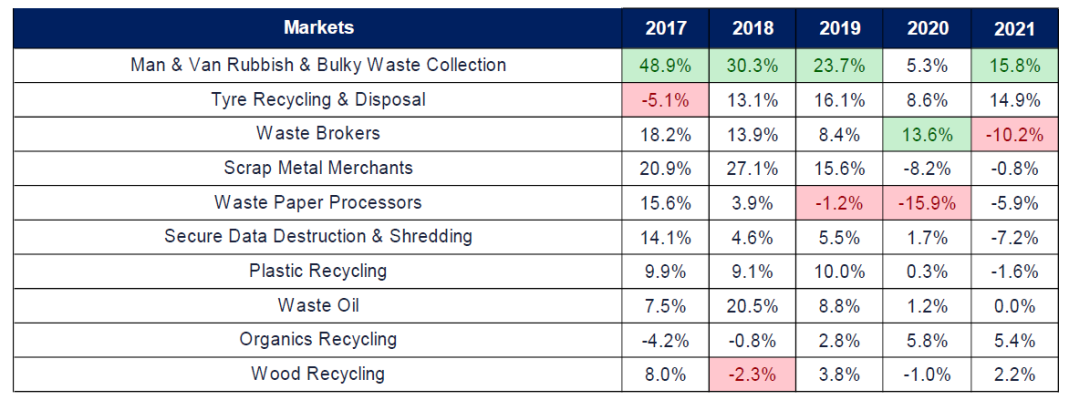

The final area worth mentioning is the niches within the wider sector. There is a sharp contrast in fortunes depending on the waste being processed. Man with van & bulky waste collection alongside Tyre Recycling & Disposal are the niches within the waste management seeing double-digit growth in business values. Elsewhere, Waste Paper Processors and Secure Data Shredding have seen the biggest falls; both average more than 6% declines.

It is clear that the waste management industry is under increasing pressure but there are pockets of sustainable value creation. To help our listeners make sense of some of the impacts we are offering a free insight report looking at business value trends across the waste management market.

For a free copy of the latest Insights Report looking at the latest trend in values across the UK waste market, just email me at c.evans@plimsoll.co.uk and I will get that processed for you immediately.